Theranautilus Secures $1.2 Mn in Seed...

19 Nov 2024

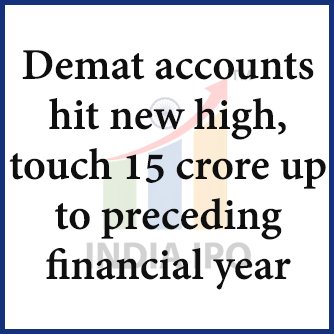

The total number of demat accounts with Central Depository Services (CDSL) and National Securities Depository (NSDL) rose by 11.9% year-on-year, reaching 15.14 crore from 11.45 crore.

The benchmark indices Sensex and Nifty50 increased by 24.85% and 28.61% respectively in FY24, while the BSE Midcap and Smallcap indices saw gains of 63.4% and 60%.

Deepak Jasani, head of retail research at HDFC Securities, attributes the surge in demat accounts to several factors: booming markets create a fear of missing out (FOMO), especially among young investors; the rising popularity of equity as an asset class; and the push by new and discount brokers to expand their customer base. This trend is expected to continue unless the market experiences a significant downturn or stagnates for a long period.

Investor interest in Indian stocks has increased as they have consistently outperformed global and emerging markets over the past five to ten years, trailing only the US. Unlike the US market, which is dominated by a few large companies, India's growth has been more broad-based.

The number of Rs 1-trillion market cap stocks has risen to 80 from 48 last fiscal year, and 250 stocks are now covered by at least 10 analysts. This expanded coverage improves earnings visibility and governance, attracting more institutional investors.

Stable inflows into equities and a more diversified market contribute to India's market stability and outperformance. However, high valuations in small and mid-cap stocks have led to many downgrades recently. Despite this, sectors such as industrials and staples have shown resilience with stable or improved ratings, according to analysts.

Global investors continue to be interested in India due to its increased weightage in MSCI indices, supportive macroeconomic conditions, growth outlook, policy stability expected during the election year, and the financialization of savings.

Request a call back

Request a call back