Theranautilus Secures $1.2 Mn in Seed...

19 Nov 2024

A vertical split replicates RIL’s shareholding pattern. For instance, a shareholder with 100 RIL shares would receive 100 Jio Platforms shares upon listing.

RIL’s promoters own 50% of Jio Platforms, while RIL holds 66%. A vertical split would thus give RIL’s promoters around 33% direct ownership in Jio Platforms.

When JFSL was listed through a vertical split, RIL’s promoters gained a 46% stake, which they have since increased to 47%. This method was favored by the market as it avoided a holding-company discount, and analysts at Jefferies India expect a similar approach for Jio Platforms.

However, this might not be straightforward for Jio Platforms, as a vertical split would give RIL’s promoters just a 33% stake, unlike the near-majority they obtained with JFSL.

Jefferies suggests raising this stake to closer to 51%, as with JFSL, but this would be expensive. Increasing their stake to 51% in Jio Platforms would require significant resources, costing around ₹1.8 trillion—18% of the promoters’ net worth.

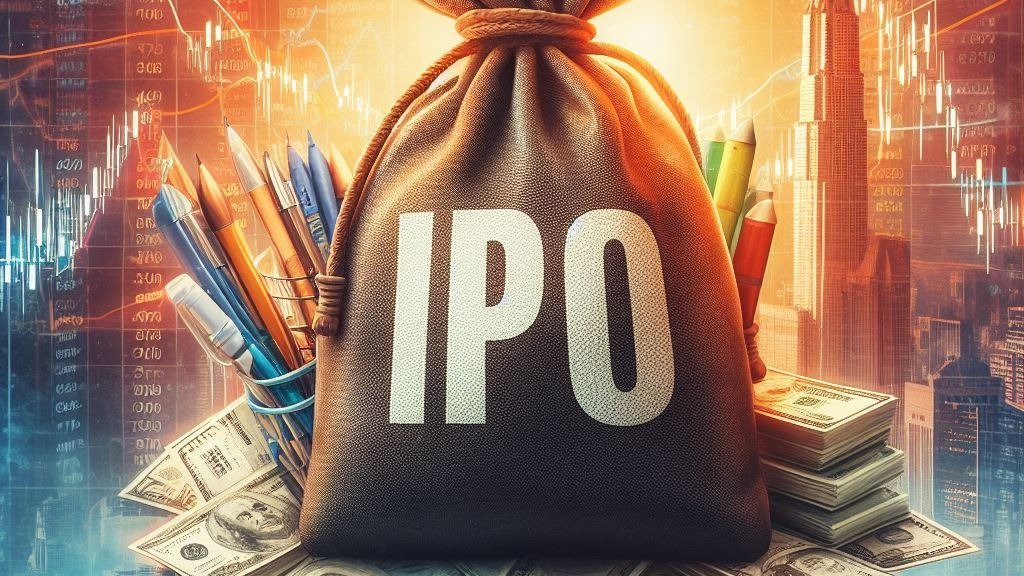

Alternatively, RIL could opt for an IPO, retaining its 66% shareholding and giving promoters more control. This might attract a holding-company discount, valued at around 20%, which would reduce RIL’s market capitalization by 5%, according to Jefferies.

Although this isn't a significant price to pay for control, filling the retail investors’ quota in such a large offering could be challenging. However, the successful IPO of Life Insurance Corporation of India Ltd (LIC) indicates a potential retail appetite of ₹14,000 crore, which is about 5% of Jio Platforms' potential market cap.

RIL, known for setting records, might manage the issue, possibly with innovative strategies like offering partly paid shares or discounts for existing shareholders. While a vertical split may be favored by investors, RIL’s promoters might choose the IPO route to maintain a controlling stake in Jio Platforms.

Request a call back

Request a call back